The crude Oil price fluctuation have been very significant since 2013, moving from a situation with a Crude oil price around USD 105 per barrel to a situation with a crude oil price falling down to USD -36 per barrel in April 2020.

The main reasons why the crude oil price have dropped under USD-36 per barrel, is mainly due to the global reserves level and the additional reserved stored in tankers, now sailing around the African continent and waiting for futur buyers in May 2020. The global oil consumption has certainly been reduced by the COVID-19 epidemical situation world-wide and the global economic slow-down since 2008 and despite the quantitive easing policies from the central banks.

The current Crude Oil price has now stabilised around USD15 per barrel in May 2020. Moving forward we should expect a Crude oil price fluctuating between USD0 and USD30 per barrel, in the best-case scenario and until the Oil consumption will increase again.

All Lockdown rules imposed by all government and the need for the global economy to resume by market and by country, should occurs with a delay linked to the nature of each business model and internal processes in place. We should expect the Crude Oil price to evolve step by step up to USD50, most likely during 2021.

The Oil commodity price situation is now challenging for the overall business model, as excluding any operating margin and consuming all cash available. This non-sustainable situation for all Oil producers market and their sub-contractors, will force the business model to be re-financed or the existing processes in place to be re-defined.

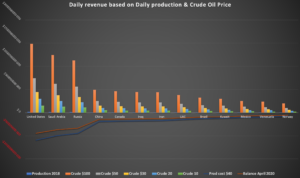

When taking a closer look at the top 10 Crude Oil producers, it is obvious that any daily production is generating a pure loss in cash, to be financed until the crude oil price will reach again the break-even price.

The table below is showing the daily loss by country, considering a production price around USD40 per barrel. In reality the production price is fluctuating depending of the type of field and location. Today the production price of one barrel of crude oil is around USD10 in UAE, around USD35 per barrel in USA, USD50 per barrel in the North Sea and can reach USD80 per barrel or more for fracking crude Oil production.

If we consider a global crude oil production reduced by 10%, the situation may end up with a revenue reduced by 10% for oil producers in middle east, and a loss reduced by 10 % for others producers with a production price above USD10 per barrel. Would a global production reduced by 10% help to bring the oil price back to USD50 per barrel in 2020?

The crude oil price evolution for H2-2020 and forward may be linked to three parameters such as the level of stocks available versus the future level of consumption and the delay for companies to resume their internal processes.

it’s important to point out here that oil fields in UAE can't be stopped and put back to productions due to the nature of the oil fields and cash available, but in others regions the oil fields are owned by small and medium size companies with limited cash available and no possibility to stop the production without losing going bankrupt. Some oil fields being stopped may never produce crude oil again.

In the airline industry, it is compulsory for the pilots grounded during 2-3 months to follow a training on simulators before working again on commercial flights. Meaning that such process may force the major airline companies to fully resume their activities not before early September 2020.

Another reason is certainly the COVID-19 pandemic situation, imposing manufacturing companies to re-think their internal QHSE processes before being able to resume their full production capacity step by step in 2020 and beyond.

The global economic slowdown during the COVID-19 pandemic situation and beyond may last for few months, until all markets will pick up again. Several companies may face cash flow issues or may have to file for Chapter 11. The lack of cash and the impossibility to re-finance a second time an accumulated debt will change the market horizon and will accelerate the closing of non-economically sustainable companies.

The remaining companies shall be a panel of public companies financed by the government and companies with a level of cash available to buffer the loss of incomes and to cover all revenues losses during the COVID-19 Pandemic situation and beyond.

The markets size, the key players and offers available may be different with a reduced numbers of offers pushing the prices up.